Rippling's Strategy to Expand Wallet Share

How They Achieve 130% NRR Selling to SMBs

This past week I had a great email exchange with a subscriber named Vincent and after a little chat recommended a few topics for me to write about that he’s been discussing recenty.

All of the ideas were great but one really stood out to me, number 2, “Strategies to expand wallet share” and one name immediately came to mind, Rippling.

So this week I’m going to dive into a few key questions:

Who are Rippling?

What are Compound Startups?

What does Rippling’s Sales Strategy look like?

It’s a longer article today because Rippling are a truly special, and contrarian company, ignoring common startup advice of focusing on one product and instead building several products in parallel that allows them to differentiate vs competitors and expand wallet share by a massive degree.

Thank you once again to Vincent and if any readers have an idea or topic they’d like to see analysed please reach out - I’d love to hear from more of you!

Intro: Who are Rippling?

Before Parker Conrad founded 2 billion dollar companies in HR he started tech life in a much less successful manner. Bored and acutely aware that he’d be in his 50s by the time he would ever get to the top of the pharma company he was working at deciding he needed to run his own thing.

Recruiting a friend they built WikInvest (later SigFig), a robo-advisor for consumer investments. However, having two CEOs at the company led to operational challenges, resulting in a split between him and his co-founder. After being fired from his own company he decided it was time for something new, so in September 2012, Parker founded Zenefits.

The idea for Zenefits came from the problem he faced managing health insurance for SigFig. Any time they needed to hire a new employee, they had to fill out paperwork to enroll in health insurance, and Parker would need to stop off at Kinko's to manually fax in the applications. He thought it was obvious this would move online.

After a troubled relationship with his co-founder he was now Silicon Valley’s golden boy. He had successfully gone through YC and reached a $4 billion valuation within just 2 years, and was one of the fastest growing startups in history, backed by the likes of a16z.

Shortly after he would get to bring on David Sacks, of the infamous PayPal mafia, as COO.

But in the desire to catch up with a lofty valuation and grow as fast as humanly possible Zenefits had let compliance slip, causing regulators to investigate the company over allegations employees were selling insurance policies in states they weren’t properly licensed.

As a result of intense media scrutiny Parker was asked to temporarily step down and let David Sacks assume an interim CEO board position to fix the compliance issues. On the condition they’d release a joint press statement and Parker would be back in 6-12 months the founder finally relented and stepped down.

Before this could ever happen Parker watched in horror as Sacks released his own statement, publicly blaming Parker and positioning himself as the White Knight of compliance.

In the months after, he continued watching as Sacks cut projects and fired large swaths of staff to optimise for cash flow and reduce compliance risk rather than grow the startup. Whilst former investors had little faith he had the ability to run another startup this was the step too far and got on the phone with Prasanna Sankar, a Zenefits employee who had emailed Parker asking to co-found his next startup.

This time around, Parker had a significant advantage: his experience at Zenefits gave him a clear view of the inefficiencies within the HR business. The fundamental problem was that almost every business system companies use is full of information about employees, and that info needs to be maintained and updated. As a result, companies would have large checklists of things they needed to do every time they would hire someone, and Parker realized that while Zenefits was only targeting a small fraction of it, no one was trying to take on the whole thing.

Launched with payroll, HRIS system, device management, single sign-on, and identity, Parker had founded a unique wedge to get companies into using Rippling. Once they were onboarded, Rippling could make way more money off a single customer because they bundled so many solutions. In order to succeed in this industry, he realized you needed to build a compound startup.

What is a Compound Startup?

The idea for Rippling is something called a compound startup, building multiple deeply integrated product lines in parallel that seamlessly work together.

Conventional wisdom on how to build a company is to focus really narrowly and build one great product but Parker thinks this is wrong. He believes that to tackle the most complex and deep-rooted issues in a business requires building a compound startup, and sees a few inherent advantages:

Compound Startups can Solve Deeper Business Problems: Regular point-solution businesses are contain to one vertical or business system whilst a lot of the deepest problems businesses face span multiple systems.

Deeply Integrated Products: By building integrated products you can actually make a 10x better product that previously wasn’t possible.

Shared Components: Rippling can spend 10x the time building common components like reports/analytics, workflow automation and role based permissions and thus make significantly better versions than SMB startups that don’t have much time to invest here.

Shared UX: Having multiple Ripping products means a consistent user experience where consumers don’t have to go through constant new implementation and training, thus costing the business money

Pricing Advantage: Compound startups can optimise over a bundle of multiple SKUs and don’t need to extract as much $$$ from a single product (Microsoft is the canonical example, bundling products like Teams into the suite to blow past Slack)

Blue Ocean: In the last 15 years many ideas for point-solution SaaS products have been picked over. Solving these deeper business problems spanning multiple systems is a much less explored area.

Consider the process around onboarding a new remote employee: companies must register tax details, ship provisioned devices, set up accounts across communication tools like Slack, Zoom, Github, and more. Once working, there's benefits administration, regulatory compliance, security policies, and other fragmented processes. When offboarding, devices must be recovered while following employment laws.

Since employee data lives across dozens of systems, point solutions cannot solve remote employment holistically – they only solve symptoms, not root causes. Companies must either pay the administrative tax to support a remote team, or miss out on top global talent.

Rippling attacks this from a fresh angle - by starting with the employee record as the core data backbone. By having a central store of each employee's role, compensation, credentials and other details, Rippling can then develop integrated solutions spanning payroll, IT, security and other areas.

These workflows are otherwise nearly impossible to execute: for example, Rippling customers can configure custom workflows that allow salespeople to give customer pricing discounts based on their level within the org. Or ingest Zendesk tickets to see payroll costs per support ticket resolved. Or run reports across silos of business data. In other companies this just isn’t possible because all the point solutions don’t talk to each other deeply enough.

What does their sales strategy look like?

Most startups follow a pretty predictable pattern. Raise a small amount of venture money and build a piece of software targeting startups and SMBs due to the shorter sales cycles vs enterprise.

If you’re one of the lucky ones your product will start to show success and several other competitors will flood into the market so you raise more and more capital. You and your competitors will begin to saturate the core market, and as a result new customers will become more and more expensive to acquire and likelier to churn as they don’t fit your core ICP.

To counter this and make your unit economics work you decide to move upmarket, into mid-market or even enterprise (2,000+ employee companies). This enables you to hire larger sales teams because the ACVs are so much larger and begin working on the features required by these larger companies like permissioning, slowing down product development work on the core product.

The reason this cycle plays out so often and causes software companies to go up-market is that the vast majority of startups struggle to run a profitable sales-led motion to SMBs where ACVs are typically low and churn is high.

Rippling’s approach instead, in stark contrast, stays firmly focused on SMBs through a sales-led approach. You submit a form and then they pull you into a discovery call to try and figure out which one of their many products you need.

The reason Rippling stay focused on SMBs is that enterprises are actually a very small slice of the market. Around 90% of people work for companies with fewer than 2,000 employees and in Canada and the UK this number is closer to 99%, and so Rippling choose to increase the average amount they can make from the larger SMB market, selling a suite of products and often have very high wallet share even though single products are largely affordable.

The other unique benefit to Rippling’s approach of 30+ product suite is that whilst businesses are rarely looking to replace all HR, IT, and payroll solutions at once, each time a small business is in market for a specific piece of software it gives Rippling another opportunity to get in the door.

Whilst customers will likely enter the discovery call with a very narrow and opinionated view of what they’re shopping for this human, sales-led approach enables Rippling to educate buyers about the deeper business problems they are facing to sell multiple SKUs on Day 1.

“Hey look, you think you’re coming to us with this one problem (e.g. setting up new joiners in slack, email, salesforce and GitHub and solving the administrative pain around that) but actually the problem you have is the fragmentation of employee data across all the business systems in your company and so they need to convince you the problem you’re seeing is a symptom of this deeper underlying disease and I can point to like 20 other problems that you have in these other areas (e.g. payroll & HR) that stem from the same underlying condition and if you are willing to solve this problem at a slightly more fundamental level Rippling can actually solve all of that for you.” Parker Conrad

This compound startup strategy then enables Rippling to press their advantage over competitors having to focus upmarket in 4 key ways, generating far higher win rates than industry averages, thus getting their foot in the door:

Human led sales which is more consultative

Rippling reps can maximise for the total bundle price vs single solutions meaning deep price discounts on bundles. Why pay $30 per employee per month for five different products ($150) if you can get a comparable offering in a single bundle for $50? This is one of the few true accumulating advantages in software – amortizing S&M across several products means you can charge less while making more.

Integrations enabling greater products

10x better middleware (e.g. role based permissions)

This strategy has a huge and rare positive feedback loop selling larger overall deals and generating highly anomalous ACVs vs the rest of the industry’s point solutions allowing their support and marketing motions to work at the lower ends of the market. On Day 1 a new Rippling customer will buy 7 SKUs whilst building deep lock-in and generating far higher ACVs than point-solution competitors.

Once they are able to get their foot in the door their advantages keep compounding, where they become an approved software vendor for the customer and allow their deeply integrated products to speak for themselves, generating high NPS scores significantly reducing the effort for future cross-sell motions.

Note: With this approach there’s a bit of a delicate balance. You don’t want to try and sell too many point solutions on Day 1 as this will likely require a greater number of approvals from different business departments within the company and slow down the process but still needs to be enough ACV for you to be profitably running a sales-led motion. Never try and rip out entire enterprise workflows, instead picking specific points to attack.

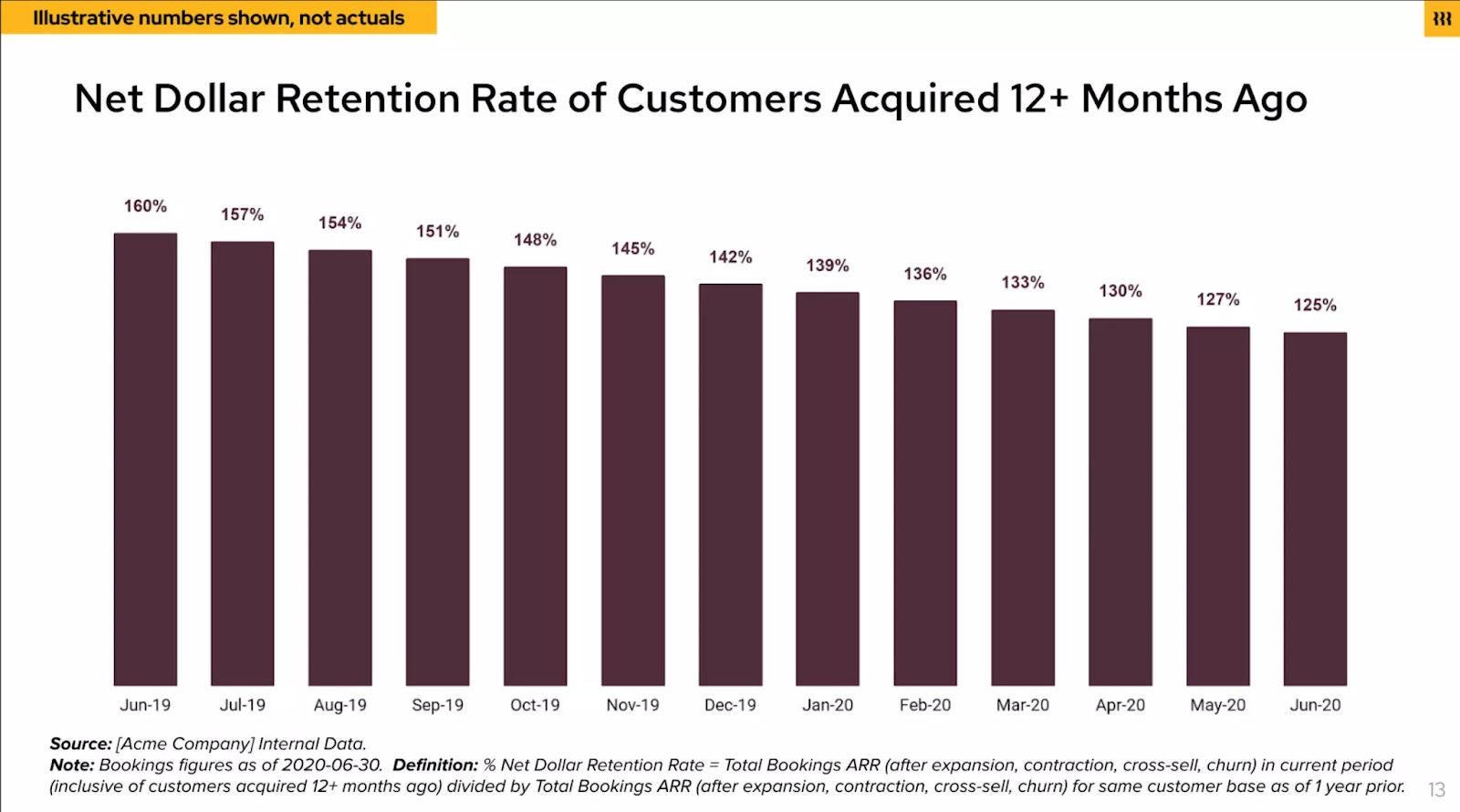

Where Rippling really set themselves apart from other SMB software providers, however, is their NRR as a result of their cross-sell motion once they’ve made this first purchase.

“Accumulating advantages are rare in software. Bundling is Rippling’s accumulating advantage that offsets classical diseconomies of scale. This means that, unlike most growth-stage companies, Rippling’s core metrics improve over time. CAC paybacks decrease. Growth accelerates. Retention improves. Cross-sell rates increase.” John Luttig, Founder’s Fund

From what we know Rippling’s NRR is around 120-130%, well above the industry average of 80% for SMB software providers led by this multi-product suite: companies start with a few product, but will naturally buy more over time.

“Once customers know you’re a multi-trick pony, they’ll start looking to you for new product offerings. Today, Rippling’s product launches are nearly guaranteed to succeed given its existing distribution and customer trust. New offerings have revenue and engagement metrics within months that most startups would be excited to reach in years. The extreme version of this is Microsoft Azure: cross-sell was how it built the fast growing b2b business of all time.’ John Luttig, Founder’s Fund

But it’s not only the top-line NRR number that’s important. Building a bundled product suite has massive sales and marketing efficiencies. A number I often quote to clients is that whilst the typical cost to acquire $1 of new customer revenue is $1.13 (e.g. it takes a little over a year to pay back the investment cost) cross-sells and renewals are vastly cheaper are vastly more efficient at $0.27 and $0.13 respectively.

The big companies understand this well, Salesforce, UI Path, PagerDuty and more all have 70+% revenue growth coming from existing customers but until Rippling it’s been impossible to achieve this in SMB. That’s what a compound startup enables. These customers know you, and as competition inevitably increases across every market why not leverage your advantages and sell to existing customers that are 5x easier than new ones?

But trying to sell a suite of 30+ products is hugely complex . Product owners would need to push marketing to highlight their product, train the sales team on selling their unique differentiators and trade-offs vs competitors, and work with the infra team to ensure the backend supports their needs. Even if product owners could accomplish this sales teams would quickly begin to get frustrated being yanked into constant training sessions for new launches and would never have the mental capacity to learn how to sell every single SKU (Rippling aims to launch 5 new products per year) in a clear way to consumers.

As a result, Rippling now have independent sales orgs, each one responsible for cross-selling these SKUs to existing customers and selling new customers.

The benefit of this is that individual sales orgs can go far deeper on that individual product (therefore getting some of the benefits of a point solution company around focus - e.g. the VP of sales just thinks about specific point solution competitors all day long, how to beat them and attack the market the right way vs a VP who has to try and figure out how to sell 30 different SKUs - they’ll instead pick the 3 or 4 that are the easiest to get to quota leading to the majority just getting ignored).

This strategy has worked increasingly well. As of mid-2023 despite serving SMBs in a tough macro-environment with 10% seat contractions on average Rippling is seeing NRRs of 130% and are booking more than $5 million/month in net new revenue from their cross-sell motion.

The final point to make it that by interlocking products it means if customers do ever become unhappy with Rippling they often can’t just taken out one SKU, it would require them to rip out their entire paywall, HR, and IT solutions and rebuild with 20-30 different vendors which would be a nightmare lasting 2+ years from a software analysis and procurement perspective.

That’s it for today folks, hope you enjoyed this longer post. Will see you again next week for a special announcement!

HB